“You know, the right way to get paid is a good spreadsheet to track overdue invoices, that’s all you need. We don’t need your product, Thank you”. I can still remember the senior CFO of a famous consulting company telling me this, as we were trying to sell Upflow to our first users in 2018. Fast forward, 4 years later, we’ve been working with hundreds of CFOs in the US and EMEA, across multiple industries and business stages. Our cash collection platform is used by hundreds of finance teams globally, and it’s now processing more than $10bn worth of invoices a year. It’s been an interesting journey, and we’ve learned a few things about finance processes along the way.

What’s fascinating about finance is that there are very few standardized playbooks in comparison to other professions. When you think about sales, marketing, or product, they can all rely on a playbook with best practices to scale. For finance professionals, that’s not yet the case. Communities are not that visible, and it’s hard to find the “standard” process or tool when you do have a question. As a result, the CFO oftentimes finds herself reinventing the wheel, trying to discover what works and doesn’t work, and learning along the way.

When it comes to Accounts Receivable (or AR) management in B2B, we've probably seen it all. From disorganized teams with no process in place to the most sophisticated teams thinking of this as a science. There are several ways to collect cash and get paid as a business. For the CFOs and finance professionals out there looking for help, this article will attempt to give you a playbook for your cash collection. Let’s get into it.

What is cash collection?

Cash collection refers to the process of collecting payments from your customers. In this article, we will cover the later part of the order-to-cash cycle, after the billing has occurred and up until the payment is recorded in your accounting ledger.

Don’t get us wrong, billing is not that simple. We’ve seen many companies failing at building their billing “in-house”, and we always urge them to rely on software to do so. Lago is one of them and here is what they have to say about it:

"Lago helps B2B companies automate their billing processes, whether their pricing is subscription-based, usage-based, or (most of the time) a hybrid grid with a high number of custom plans and exceptions. Once we’ve automated billing, our first recommendation is: ‘Take care of cash collection, it’s not trivial. We’ve made sure you bill your users the right amount, and in a compliant way, now the hardest is to make sure you collect that cash on time’."

Anh Tho Chuong Degroote, cofounder at Lago

Indeed, one can think that once billing is completed, the job is done. Right? But that is not exactly the case, as your customers still have to make the payment - and unfortunately in B2B, it’s not that straightforward. You may offer different payment terms, payment methods, and currencies. Some customers will pay you on time, some will just forget. Some will try to optimize their own cash flows by not paying you at all. Even once you are paid, the cash application process (i.e. linking the payment to the corresponding outstanding invoices) can quickly turn into a nightmare with large transaction volumes The icing on the cake? The process involves customers (a.k.a the King). This means that you need to maintain a good relationship whilst navigating a sensitive topic. If you don’t know what I am talking about, try sending out a reminder to a customer who’s already paid. I bet they won’t be too happy about it.

A revolution is coming in B2B payments, are you ready or late?

B2B cash collection hasn’t really changed in the last few decades, despite its revolution in all other payment verticals (retail, consumer, online to name a few). Using a check (yes, a piece of paper) to process a payment, or manually entering payment information on an outdated bank interface is still commonly accepted in 2023. This probably won’t be the case in 2030. Just because, a piece of paper in an envelope with your signature on it can’t be the future of payments. And as our old favorite CFO above, many finance professionals use spreadsheets to cover the lack of tools.

So, how can you optimize this process to not only streamline cash collection but also be an early adopter of these upcoming changes? You first need to understand the different stages of maturity of this cash collection process and use it as a framework to progress over time in your finance function.

The 5 maturity stages of cash collection

At Upflow, we’ve developed a framework by identifying the 5 main stages of cash collection maturity. Some may argue that there are more steps or fewer steps and that each of them may be covered in more depth. Don’t get lost in the details, let’s focus on the bigger picture first, and we can cover each of them in more detail later.

Step 1: Measuring real-time AR data

You can’t improve what you don’t measure. True! So let’s start here.

Too often, we meet with finance teams who don’t have access to real-time AR data, i.e. they don’t really know which customer has paid them. It seems quite basic, but there are often delays in recording the payment when done manually, and this information usually stays within the finance team and is not shared with other business stakeholders. Knowing the payment status is basic, and as usual with data, you can track many financial KPIs to go a deeper analysis.

Keep it simple to get started. We would recommend keeping an eye on these 3 key indicators:

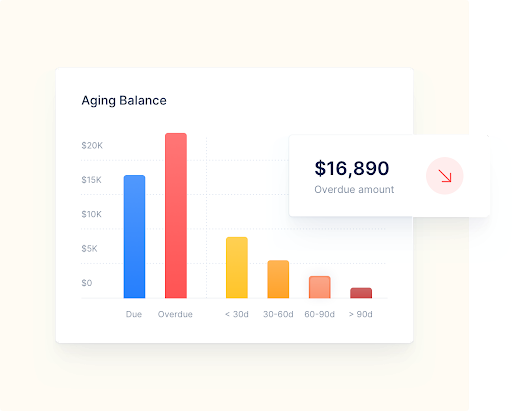

Your aging report. It will quickly give you a sense of the health of your accounts receivable. If it’s skewed towards the right/older buckets, then it’s not a great sign.

Your day sales outstanding (or “DSO”). Compare it to your default payment terms. If it’s 30% higher than your standard payment terms, there is probably an issue with your ability to collect money.

Your billing cohorts and write-off rate. That’s how fast you collect and what’s left unpaid after 6 months. If it’s consistently higher than 2%, then it’s time to revisit your process.

As your business keeps on growing and you’re sending out more and more invoices to many different customers, you may want to get more sophisticated. You may wish to slice and dice that data: filter it by segment, and business units, using benchmarks. Just remember that doing it rather than getting it perfect is a step in the right direction.

Whatever you measure, try to get it on time (i.e in real-time, not when your accountant closes the books 6 months later) and share it with the right people (i.e the business team). Your VP of Sales should quickly know they’re selling to bad-paying customers. So should your CEO! We will take a closer look at how you can perform collaborative cash collection with your team in step 2.

Let’s face it, B2B companies are usually bad at cash collection. What’s worse? They don’t even know that they are! Don’t be that company, get in the know now.

Step 2: Setting up a systematic process with your team and your customers

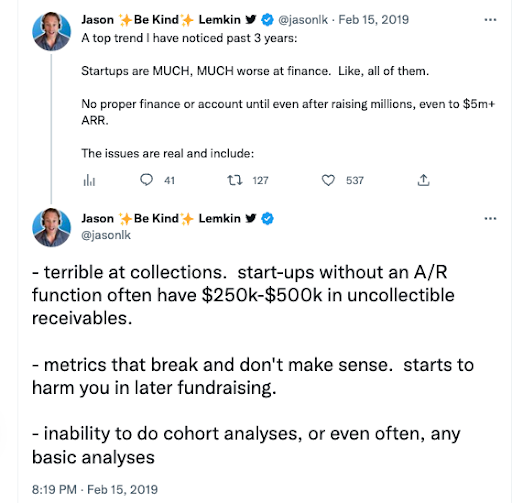

Now that you know you have a problem, it’s time to fix it. The good news is that: most customers want to pay you. People are often surprised when we state the obvious, but that’s just the way it is! Otherwise, you wouldn’t have a business. Our benchmarks show that 70% of unpaid invoices are related to technical issues, such as deliverability issues, missing validations, and payment method issues. If you let those issues fall through the cracks, then you’ll end up with late invoices and write-offs which will hurt your business even more, not only through lower cash collection but also involuntary churn, as described by GoCardless. Don’t let this impact your cash flow.

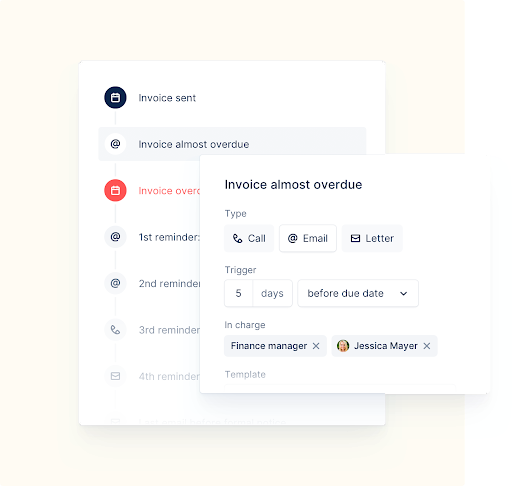

So your immediate goal is the following: do not let anything fall through the cracks. Be proactive. Make your customer's life simple. Have payment information readily accessible. Reach out to the right contacts. Make sure your customers have a simple way to communicate their issues with you as soon as possible.

If you issue a few invoices a month, then a spreadsheet will do. But if you start sending hundreds of invoices per month, you 100% need to set up a systematic approach using a dedicated tool. We call this a workflow. It can be automated for small customers, but you’ll probably need some additional context for larger ones.

That’s where things can become complicated, as you need to bring in the right people on your side (sales, success) and on the customer side (finance, account manager) with the right commercial context. You will need to cross data from your CRM and your billing tool to achieve this.

This seems very complex, but if you get this right, you will already be in a good spot on what matters most: making sure bad debt is under control. That’s what matters for your cash in the bank.

Step 3: Enabling new payment methods

Ok, if you’re past step 2, you’re already better than 80% of the finance teams we see out there. I mean it.

But not only do you want to collect all of your cash, but you also want to collect it faster. This is where payment methods come in.

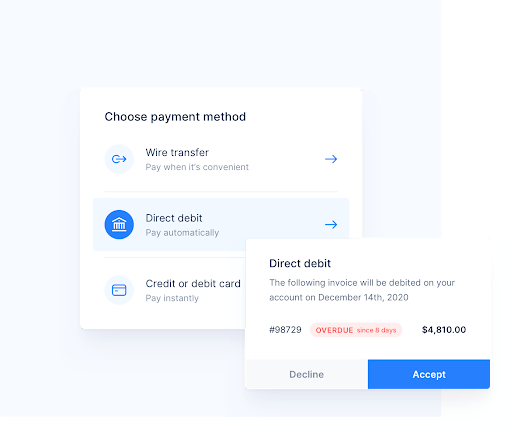

Keep in mind that payment methods come in 2 large categories:

Push payment methods. You wait for your customer to pay you (check, wire for example).

Pull payment methods or “autopay”. You charge or “pull” money from the customer's bank account. You may even do this the minute the invoice is due. Cha-ching!

Have you ever sent a check to Netflix or Spotify? Nope! In the consumer space, nearly every vendor pulls money from you. All subscription businesses do. And all modern B2B companies should do the same. Now is your turn to shine!

You may think this is impossible. But if Carta, Salesloft, PayFit, and other great tech companies do it you can do it too! Or at least give it a try. Whatever % of your collection is charged is a little less of a headache, and a little more predictability. Set expectations early with your customers: sit down with your VP of Sales and make sure every contract now involves a default autopay payment method. If you do this upon signing, you’ll get less resistance from customers.

In general, try to think about your billing process as a checkout and a funnel, i.e. a step-by-step process, in which you are trying to optimize the conversion from the first step to the next, up until your desired objective (here, getting paid). The more “Pay” options you have, the better the conversion rate to timely payment and the better your DSO. If you grow fast, the impact on your working capital requirement can be significant.

"At PayFit, the Quote to Cash process has always been a major focus, with three key requirements: automation, performance, and customer satisfaction. For a long time, direct debit was our only payment option in EMEA, as it fully met our requirements, while facilitating cash flow predictability and optimizing collection costs. As we moved upmarket, we had to offer other payment methods, but by far our payment mix remained direct debit, which helped us maintain high collection ratios."

Francis Saillard, ex CFO at PayFit

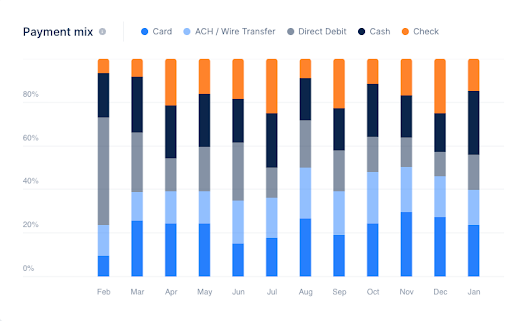

Step 4: Optimizing the payment method mix

Now that you have several payment methods available, you’ve probably achieved some improvements.

Maybe some customers are happy with money being directly charged to their bank account.

Maybe some have agreed to jump into the 21st century and wire you money rather than sending you a check at your outdated office address.

Maybe some payments are automatically applied to your open invoices rather than manually, and you’re able to have live AR data with no effort.

That’s great news. Looking at the analytics you’ve built in step 1, you now have a good understanding of your payment mix, i.e the split of how you collect your revenues per payment method. Each of them has its own pros and cons. Some are more predictable than others, some are more expensive.

So you can now try to optimize the payment mix with 2 main goals in mind:

Increasing your cash collection speed, typically by increasing the share of autopay/pull payment methods, to make sure that you’re paid on time.

Optimizing the cost of your payment mix, by replacing costly payment methods (for example credit cards on large transactions) with more cost-efficient payment methods such as ACH or SEPA direct debit.

Once you have a good understanding of your data and areas of improvement, influencing your payment mix toward favorable payment methods is not an easy task. But you can do this by following these recommendations:

Discuss/set billing and payment options during the sales process: sit down with your VP of Sales and ask her how better payment methods can be added as the default when signing up for your services. If you don’t specify anything, customers will choose. It’s easier to set an ACH debit (or SEPA Direct Debit) upon signing than after the first invoice is due.

Embed payment methods in your onboarding process: Make it easier for your customers to sign up for your preferred payment method, which will allow for better control of your cash collection. Customers tend to be more flexible upon onboarding than updating to a new payment method later down the line.

Restrict the use of payment methods for specific customers or transactions. For example, offer credit card payment for small one-off amounts, but restrict it for larger amounts to avoid large fees.

Give financial incentives to your sales team and your customers to move to other payment methods.

Make sure you offer a payment portal with all outstanding invoices and payment methods available.

Use every single communication to your customers (new invoices, overdue notices) as a prompt for setting the payment method you’ve decided to push for.

"At Carta, we’ve always had a holistic approach to our revenue generation engine and cash collection processes, with finance, sales, and customer success working hand-in-hand. This started with us thinking through our customer onboarding workflow, making it a simple and clear process for our customers, while being thoughtful about cash flow optimization. In addition to ACH debit being the default payment method at signup, we have tested new options with the business team (on payment methods, payment terms, etc.) to find ways to further optimize our cash flow.

Charly Kevers, CFO at Carta

Step 5: Financing your accounts receivable

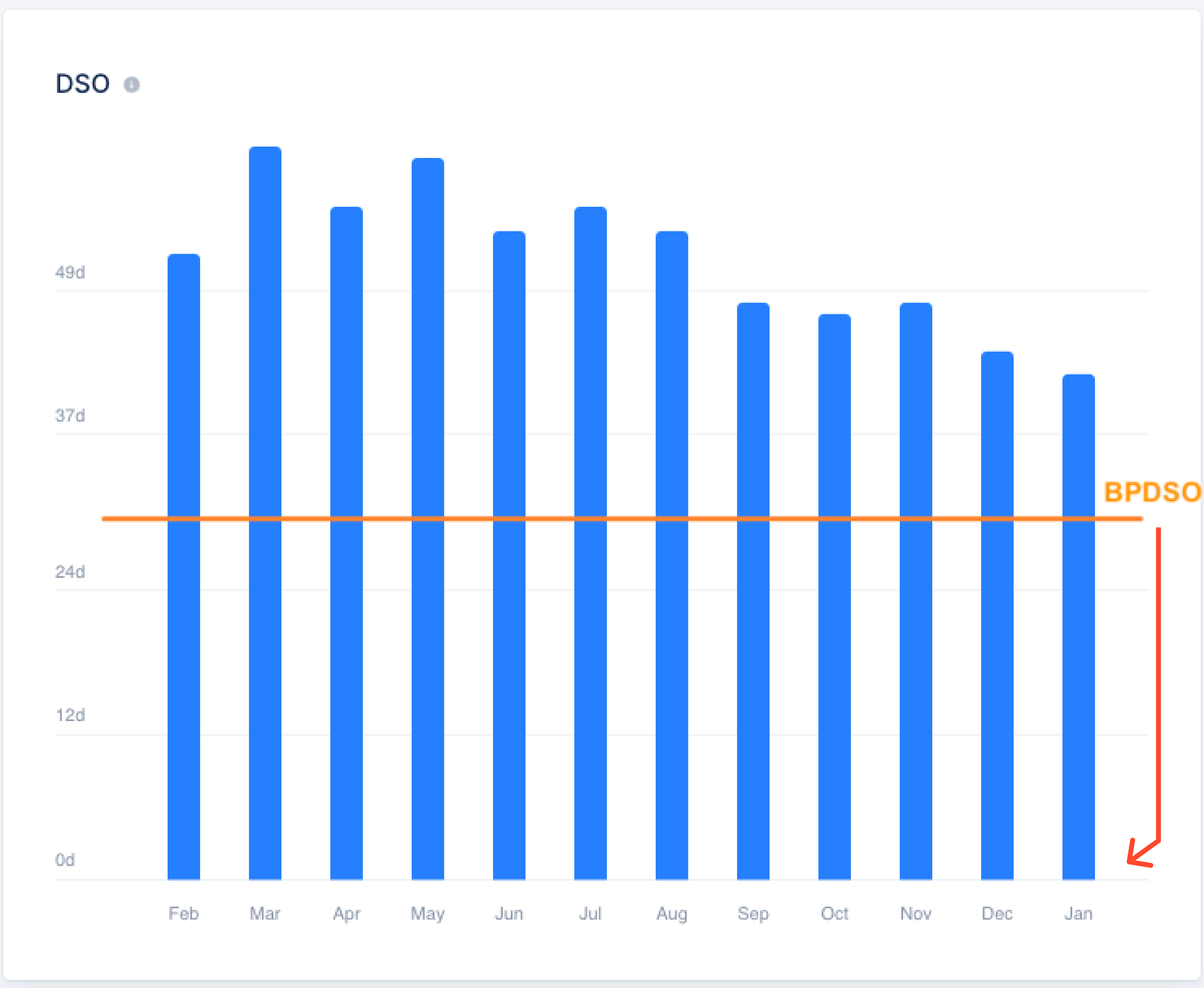

Once you’ve implemented all of those and you’ve had time to finetune these processes, your cash collection is probably the best in class. You may observe a very low rate of write-offs and a best-in-class DSO, close to what is called the “Best Possible DSO” or BPDSO. Once you’re there, there’s not much more to expect from your customers. It’s very unlikely that they will pay you before the due date of the invoice. Why would they?

This is where financing comes in. Using a bank or a specialized financial institution, you could finance this last portion of your DSO to get your money now, rather than later. In a nutshell, if your DSO was higher than your BPDSO, you’re now close to it, now you can finance the remaining portion, to collect your outstanding invoice immediately, not when they become due.

“Since credit is harder to get, cash has become the focus. As a result, cash flow management tools have never been more valuable—specifically, tools that provide insight into cash, such as predictions around who pays on time, how long the average working capital cycle is, when payment typically happens, and the terms around current credit cards or loans. This visibility is currently missing for almost all SMBs”

Seema Amble, partner at Andreessen Horowitz

There are several reasons for financing as a last step, and not as the first one:

Financing can be very expensive, so you want to only use it when needed, not to finance delays you could have fixed in the previous steps.

Financing is easier and cheaper when it’s about financing high-quality cash flows. If your write-off rate is high, it means a high probability of default, and that’s exactly what banks don’t like. Fix it first, finance it second.

If you finance low-quality cash flows, you will only postpone the issue. If you finance an invoice that is not going to be collected (for whatever reason highlighted above), ultimately you will bear its collection cost, just keep this in mind.

"As a modern lending organism, financing high-quality cash flow is the best scenario for our users and for us. It lowers the credit risk and therefore makes it more cost-effective for our users. When it comes to financing working capital through accounts receivable, if cash collection processes are not efficient, we could end up with bad debt, and the cost of it always goes back, one way or another, on our users. That’s why we always encourage finance teams to streamline their entire order-to-cash cycle rather than only one part of it."

Jordane Giuly, Cofounder at Defacto

As a finance leader, what actions should you take?

Remember our CFO at the beginning of our story? He’s now retired (and that may be better for their company). I’m sure that by now you understand that spreadsheets can barely help you achieve the most basic tracking of unpaid invoices, but not much in terms of advanced steps.

By now, you probably have a good understanding of what these stages are and the potential impact on cash collection for your business. But the real question is: where do you stand on a scale from 1 to 5? Again, remember that most companies struggle to get to stage step 2, so don’t feel (too) bad about your relative advancement. Progress matters! Keep in mind that real revenues are the ones you’ve cashed in and should be the main focus for your finance team.

Once you’ve identified where you are, you can follow the steps above to get to the next level. Just work in small increments to get started. With each step implemented, you will be able to measure the impact, see increased cash flows, and report it internally.

I've given you the 5 steps to unlock your cash collection. The ball is now in your court. Take action and you'll be well on your way to becoming a finance pioneer well ahead of the curve.

Written by Alex Louisy, CEO and co-founder of Upflow, a pioneering cash collection technology company.